In 2023, I received an email from someone who had sent A$500 via PayID to what turned out to be a fraudulent casino — a slick-looking website that vanished three days after collecting deposits. The money was gone, the operator was untraceable, and the player’s bank could not reverse the transfer because PayID payments are irrevocable by design. It was a painful lesson, and it is the kind of scenario that makes the question “is PayID safe?” more nuanced than a simple yes or no.

Payment card fraud across Australia totalled $854 million in the 2025 financial year — a figure that reflects the scale of financial crime in this country. PayID and the NPP were built with different security assumptions than card networks, and understanding what those assumptions protect and what they leave exposed is essential for anyone using PayID to fund online gambling. The technology itself is robust. The risk sits in how people use it, and in the gap between what the payment system safeguards and what it was never designed to prevent.

This is a security analysis, structured around the specific threat landscape that Australian online gamblers face when using PayID. I will walk through the protective layers — name-matching, Confirmation of Payee, bank-level monitoring — and then the gaps where those protections do not reach. The goal is not to alarm or reassure, but to give you accurate information for making your own risk assessment.

How PayID’s Name-Matching Protects Your Transfer

The first time I demonstrated PayID’s name-matching to a room of payment industry analysts in 2020, someone in the audience called it “the feature that solves the wrong problem.” He was wrong then, and the data has proved it since. Name-matching is PayID’s primary security mechanism, and it works by showing you the registered name of the recipient before you confirm the transfer.

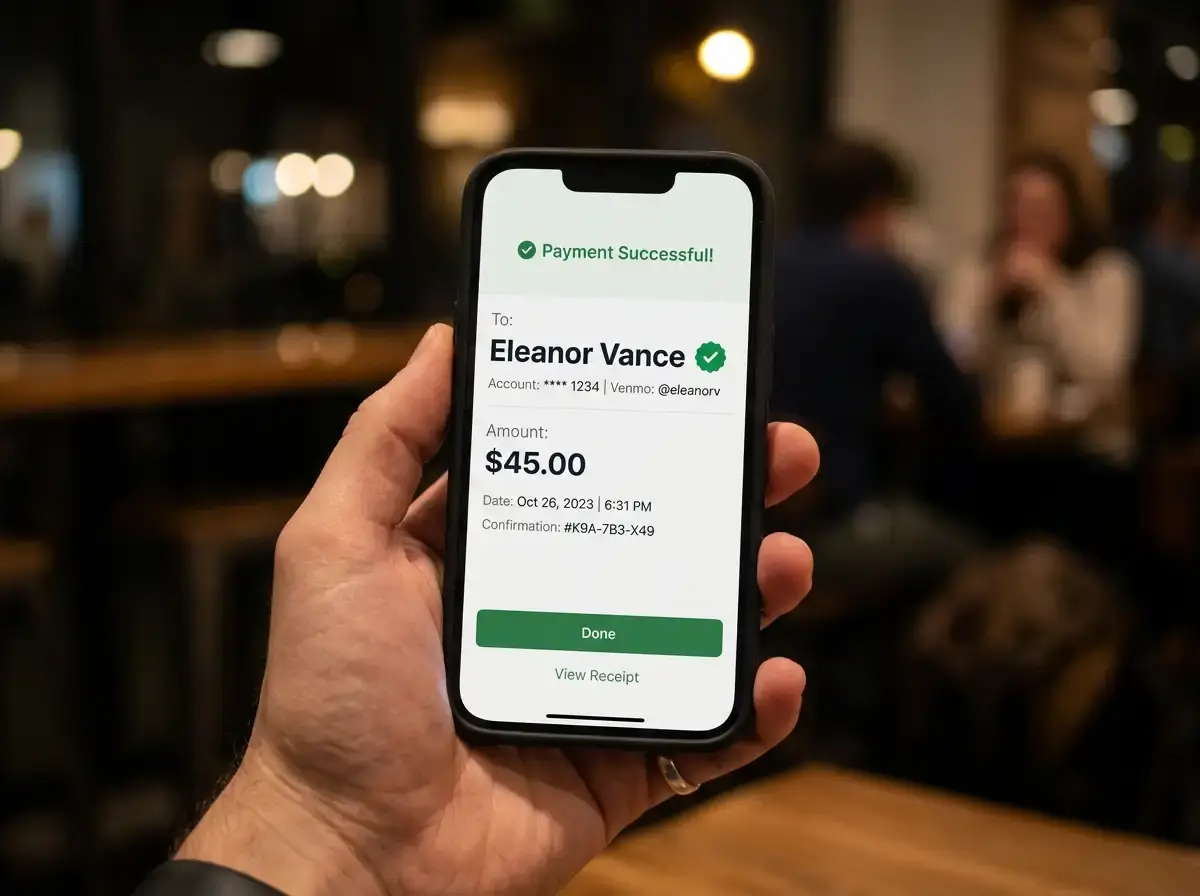

Here is what happens technically: you enter a PayID (phone number or email) into your banking app. Your bank sends a lookup request through the NPP to the receiving bank, which returns the name registered against that PayID. Your bank displays that name on screen — “You are sending A$100 to ACME Gaming Pty Ltd” — and asks you to confirm. If the name does not match what you expected, you can cancel the payment before any money moves. One in four PayID users has stopped or adjusted a payment because the displayed name did not match their expectation, preventing either an error or a potential scam.

For casino deposits specifically, name-matching serves as a first-layer verification. When you send money to a casino’s PayID, the displayed name should correspond to the casino’s registered corporate entity or its payment processor. If you are depositing at a casino called “Lucky Stars” and the PayID resolves to “John Smith” — a personal name rather than a business entity — that is a red flag worth pausing for. Legitimate operators register business PayIDs under their corporate trading names, not individual names.

Anna Bligh, CEO of the Australian Banking Association, noted that PayID’s proportion of all payments grew from 12% in early 2021 to nearly 20% by late 2022, driven significantly by the trust that name-matching created among users. That growth trajectory has continued — the feature addresses a genuine anxiety about sending money to the wrong place, and it does so at the most critical moment: before the irreversible transfer is confirmed.

The limitation is straightforward: name-matching tells you who is registered against a PayID, but it cannot tell you whether that entity is trustworthy, licensed, or legitimate. A fraudulent casino can register a convincing-sounding business PayID (“Premium Gaming Solutions Pty Ltd”) and the name-matching feature will display it without any fraud warning. The name is accurate — it is just the name of a company you should not be sending money to. Name-matching prevents accidental misdirection; it does not prevent deliberate deception.

How Confirmation of Payee Adds a Safety Layer

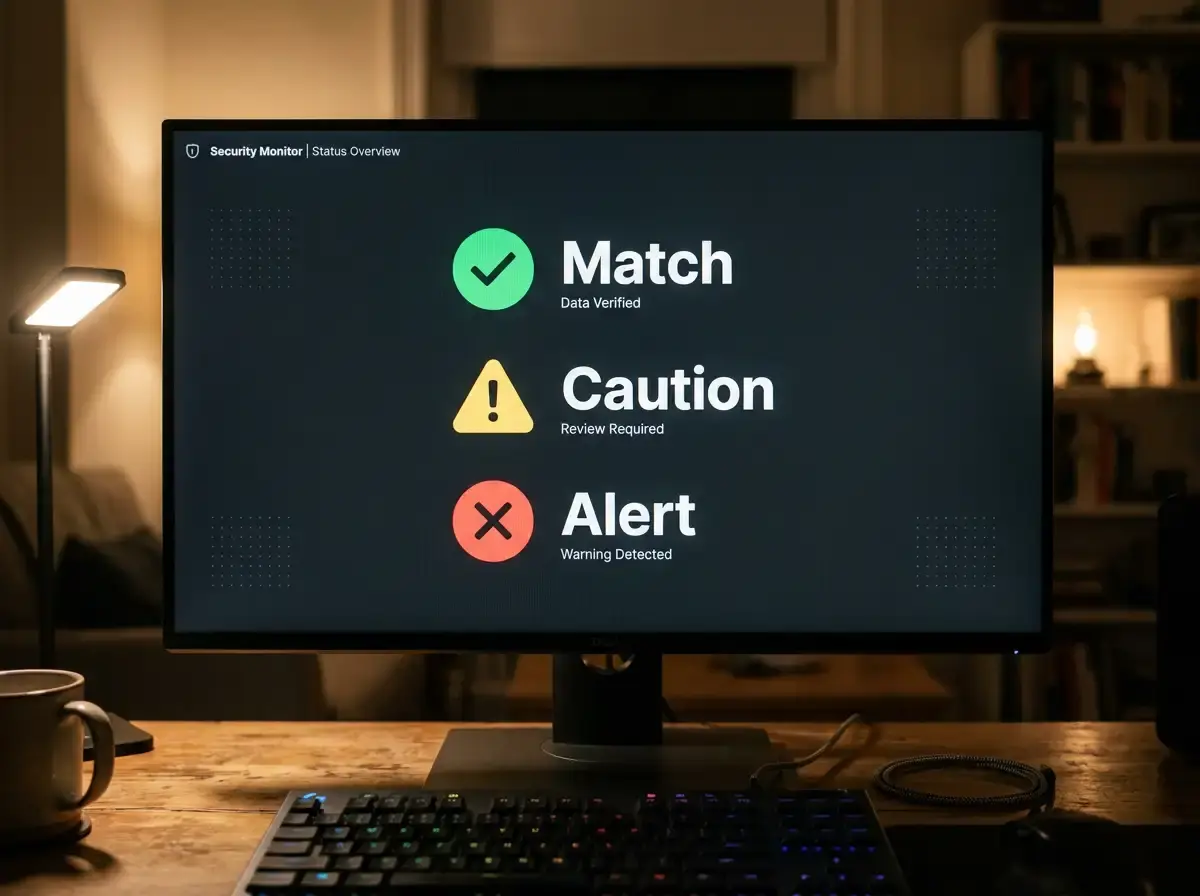

Launched in July 2025, Confirmation of Payee builds on the name-matching concept by adding active verification rather than passive display. When you initiate a PayID transfer, the system now cross-checks the name you entered against the name registered at the receiving bank and returns a match result: full match, partial match, or no match. The Australian banking sector invested $100 million in developing and deploying this technology across the entire industry.

The numbers from the first months of operation tell a compelling story. Confirmation of Payee has been used more than 100 million times since launch. At a single bank, over 450,000 payments were cancelled after returning a “no match” result — and more than 10,000 of those cancelled payments were destined for accounts flagged in the Australian Financial Crimes Exchange database. Anna Bligh described the rollout as positioning Australia among a handful of countries with this protection across the entire banking sector.

For casino deposits, CoP adds a layer of friction that is genuinely protective. If you type a casino’s PayID and the name you expect does not match what the receiving bank has registered, the system warns you before the money moves. I have covered the technical mechanics and edge cases of CoP in detail in a dedicated analysis of Confirmation of Payee at casinos, including what partial matches mean and how the system handles business-name variations.

Common PayID Scams Targeting Casino Players

I keep a running catalogue of PayID scam patterns reported by Australian players, and the three most common targeting casino users share a depressing similarity: they all exploit trust rather than technology. The NPP is not being hacked. People are being deceived into voluntarily sending money to the wrong recipients.

The fake casino scam is the most straightforward. A fraudulent operator creates a professional-looking website, advertises through social media or search ads, accepts deposits via PayID, and then either refuses withdrawals or disappears entirely. More than $45 million was lost to purchase and sale scams in Australia in 2023, with PayID-specific losses accounting for at least $260,000 in documented cases — though the actual figure is likely higher, as many victims do not report to Scamwatch due to the stigma around gambling losses.

Australian Payments Plus coined the term “scambling” to describe a specific pattern where fraudulent operators use social media ads to lure players to fake casino platforms. These ads often promise unrealistic returns or guaranteed winnings, targeting people who may not have experience with legitimate operators. The scambling pattern is particularly effective because social media platforms’ ad targeting can reach vulnerable demographics with precision that traditional advertising cannot.

Chris Sheehan, NAB’s head of fraud, highlighted a related pattern in which scammers pose as buyers on marketplace platforms, requesting a seller’s PayID to “verify” payment before purchasing an item. In the casino context, a variation involves scammers contacting players through forums or social media, claiming to represent a casino’s support team and requesting PayID details to “process a withdrawal.” No legitimate casino will ever contact you asking for your PayID information — deposits are always initiated by you, not pulled by the operator.

The refund scam targets players who have lost money at legitimate casinos. Scammers posing as “recovery agents” or “chargeback specialists” contact victims, promise to recover lost gambling funds, and request an upfront fee via PayID. The recovery service does not exist. Scamwatch data shows online contact methods were responsible for $122 million in losses during the first nine months of 2025 alone. The uncomfortable truth is that once a PayID payment leaves your account, no third party can recover it without the recipient’s cooperation.

What PayID Does Not Protect You From

A player I corresponded with in late 2025 summed up the misconception perfectly: “I thought PayID was like a credit card — if something goes wrong, the bank sorts it out.” He had just lost A$800 to an operator that closed its doors overnight. His bank was sympathetic but clear: PayID transactions are push payments, not pull payments, and that distinction changes everything about your consumer protections.

Credit cards and debit cards operate on a pull model — you authorise a merchant to pull funds from your account, and your bank can reverse that pull through the chargeback process if the merchant does not deliver. PayID operates on a push model — you initiate the transfer, you confirm the recipient name, and you push the money out. Once the funds leave your account, they belong to the recipient. Your bank has no mechanism to claw them back without the receiving bank’s cooperation and the recipient’s consent. The NPP processed over 2 billion transactions in 2024, and the irrevocability of each one is a feature, not a bug — it is what makes the system fast, final, and trusted by businesses.

This means PayID offers zero protection against operator insolvency. If a casino accepts your deposit and then goes bust, your PayID payment is not treated differently from any other unsecured creditor claim. You are in the queue behind employees, tax authorities, and secured lenders. The practical recovery rate in offshore casino insolvencies is close to zero for individual depositors.

PayID also cannot protect you from yourself. Problem gambling losses sent via PayID are not reversible — there is no cooling-off period, no pending state you can cancel during a moment of clarity. The National Consumer Credit Protection Act and the credit card gambling ban that took effect in August 2024 were specifically designed to add friction to gambling transactions. PayID, by design, removes friction. That speed is a benefit for controlled players and a risk multiplier for anyone struggling with impulse control.

Authorised push payment fraud — where you are tricked into voluntarily sending money to a scammer — sits in a regulatory grey area in Australia. The UK introduced mandatory reimbursement for APP fraud victims in October 2024, but Australia has no equivalent scheme. If you send a PayID payment to a scammer who convinced you they were a legitimate casino, your bank is not obligated to reimburse the loss. The bank you choose matters for customer service quality, but the legal protections are the same across all institutions: minimal for voluntary push payments.

Practical Safety Checklist for PayID Gambling

After years of testing operators and documenting the gaps in PayID’s protections, I have distilled what works into a set of practices that take about ten minutes to implement and cost nothing. None of them are complicated. The challenge is doing them consistently rather than skipping them when you are eager to start playing.

Start with a dedicated bank account for gambling transactions. Every major Australian bank lets you open a secondary account through your existing app in minutes, and most do not charge monthly fees on basic transaction accounts. Move your gambling budget into this account via internal transfer, then use its PayID for casino deposits. This achieves two things: it caps your exposure to whatever balance you have deliberately allocated, and it keeps gambling transactions separate from your primary financial records. If a casino’s PayID is ever compromised and used in a social engineering attack, the exposed account holds only your discretionary gambling funds, not your salary or savings.

Before your first deposit with any new operator, run the PayID name check without completing the transaction. Enter the casino’s PayID in your banking app, let the name-matching result appear, and photograph the screen. That screenshot becomes your receipt proving the registered entity behind the PayID at the time of your deposit. If a dispute arises later, you have documented evidence of who your bank identified as the recipient.

Set daily PayID transfer limits through your banking app. Most banks allow you to configure per-transaction and daily cumulative limits independently of the bank’s default caps. A daily outgoing limit of A$200 or A$500 — whatever matches your actual gambling budget — creates a hard stop that no amount of tilt or chasing can override in the moment. You can raise the limit later if needed, but the friction of changing a setting during an emotional state is often enough to break the impulse cycle.

Enable transaction notifications for your gambling account. Real-time push alerts for every outgoing PayID transfer create an automatic audit trail on your phone. More importantly, they make every deposit a conscious event rather than an invisible background action. The 155 million monthly NPP transactions process silently by default — adding notifications ensures yours do not.

How to Identify Unlicensed Casinos Before You Deposit

Here is something that surprises people when I explain it: the vast majority of online casinos accepting PayID deposits from Australians operate without an Australian licence. That is not inherently illegal for the player — the Interactive Gambling Act 2001 targets operators, not individual bettors — but it means the regulatory protections you associate with licensed gambling do not apply. No state-based consumer complaints process, no responsible gambling interventions mandated by law, no requirement to segregate player funds from operating capital.

The distinction between “unlicensed but operational” and “unlicensed and fraudulent” is where your due diligence matters. An offshore casino holding a licence from Curaçao, Malta, or Gibraltar operates under a different regulatory framework, but it does operate under one — with varying degrees of player protection depending on the jurisdiction. A casino with no licence from anywhere is answerable to nobody, and that is the category you need to identify and avoid.

Check the website footer for licence information. Legitimate offshore operators display their licence number and issuing jurisdiction, typically with a clickable verification seal. If the footer contains no licence reference, or if the seal links to a dead page or an unrelated website, treat it as a warning. Cross-reference the claimed licence number on the issuing authority’s public register — Curaçao’s is searchable online, Malta Gaming Authority publishes a complete operator list, and Gibraltar maintains its own registry.

Examine the casino’s payment infrastructure. Operators using PayID typically partner with a payment processor that handles the NPP integration rather than connecting directly. If the casino cannot name its payment processor, or if the PayID resolves to a personal name rather than a business entity, the operator is either extremely new or deliberately obscuring its financial structure. Neither scenario favours the player.

Search for the operator’s corporate registration. Australian-facing casinos often incorporate in jurisdictions with public company registries. A company registration number, a verifiable trading address, and named directors are baseline indicators that a real business exists behind the website. The absence of any corporate transparency — no registered entity, no physical address, no identifiable ownership — is the single strongest predictor of a fraudulent operation in my experience testing PayID casinos over the past four years.