Let me start with a confession: I have a folder on my desktop labelled “withdrawal receipts” containing 47 screenshots from the past eighteen months. Each one documents a real withdrawal test at a different PayID-accepting casino — the request timestamp, the processing notification, and the moment funds actually appeared in a bank account. The gap between what casinos promise and what they deliver is the entire reason this article exists.

“Instant withdrawal” is the most abused phrase in online casino marketing. Search for PayID casinos and you will find operator after operator claiming instant or near-instant payouts, often in bold text next to a lightning bolt icon. The reality, documented across those 47 tests, tells a different story — one involving internal processing queues, identity verification delays, and the uncomfortable truth that most PayID casinos do not actually process withdrawals through PayID at all.

This is a fact-checking exercise, not a promotional guide. The NPP infrastructure that powers PayID can absolutely move money in seconds — it handled 1.6 billion transactions worth AUD 1.99 trillion in 2024 alone, a 23% increase over the previous year. The technology is not the bottleneck. The bottleneck is everything that happens between you clicking “withdraw” and the casino initiating the transfer. Understanding where the delays actually live — and which ones you can influence — is the difference between realistic expectations and frustrated refreshing of your banking app.

The “Instant Withdrawal” Claim: Marketing vs Reality

I keep coming back to a specific casino landing page I archived in early 2026. The headline read: “Withdraw Your Winnings Instantly With PayID.” Below it, buried in the terms and conditions, was this line: “Withdrawal requests are processed within 1-3 business days.” That is not a contradiction the operator was unaware of — it is a deliberate marketing strategy that exploits the gap between a payment method’s technical capability and an operator’s internal processing speed.

The word “instant” in casino marketing almost never refers to the total time between clicking “withdraw” and seeing money in your bank account. It refers specifically to the final leg — the payment transmission after the casino has approved and processed your request. PayID and the NPP can indeed settle that final transmission in seconds. But the final transmission is the shortest part of a multi-stage process, like boasting about the speed of a courier who only picks up the package three days after you dropped it off.

A typical withdrawal at a PayID-accepting casino passes through four stages. First, you submit the request through the casino’s cashier interface. Second, the casino’s compliance team reviews the request — checking your identity verification status, reviewing wagering requirements, and sometimes applying manual fraud checks. Third, the finance team batches approved withdrawals and initiates the actual payments, often at fixed times during the business day. Fourth, the payment travels through the banking system to your account. Only that fourth stage is “instant” when PayID is involved. Stages two and three are entirely controlled by the operator, and they are where days disappear.

One in four PayID users has stopped or corrected a payment thanks to the name-display feature that shows the recipient’s registered name before you confirm a transfer. That protection works in both directions — it is useful when depositing to verify you are sending to the right entity, and it is relevant on the withdrawal side because any discrepancy between the name on your casino account and the name on your PayID can trigger additional verification steps that further delay the payout.

The gap between marketing and reality is not unique to PayID casinos — it exists across every payment method. But PayID’s instant deposit experience sets expectations that the withdrawal experience cannot match, creating a frustration asymmetry. Depositing A$100 takes 45 seconds. Withdrawing A$100 might take 45 hours. That contrast is jarring, and no amount of fine print prepares a player for it the first time.

Why Most Casinos Cannot Process PayID Withdrawals

This is the question I get asked more than any other, and the answer requires a detour into how PayID actually works at the infrastructure level. PayID is an addressing layer — it maps a memorable identifier like a phone number or email to a BSB and account number held at an Australian financial institution. When someone sends money to your PayID, the NPP resolves the identifier to your bank details and routes the payment. Simple, elegant, fast.

Now consider the position of an offshore casino operating from, say, Curaçao. To send a PayID payment to an Australian player, that casino would need to originate an NPP transaction — which requires being a participant in the NPP network, either directly or through an Australian banking partner. Most offshore operators do not have Australian banking relationships at all. They operate through international payment processors, correspondent banking chains, and sometimes cryptocurrency rails that sit entirely outside the Australian domestic payment infrastructure.

Even the handful of casinos that maintain Australian bank accounts for receiving deposits face obstacles on the withdrawal side. Sending bulk payments to hundreds of individual PayIDs triggers anti-money-laundering monitoring at the bank level. Australian banks have become increasingly aggressive about scrutinising gambling-related transactions since the updated AML/CTF Amendment passed in late 2025, with penalties reaching up to AUD 2.2 million per violation for corporations. A casino making dozens of daily outbound payments to individual consumers looks, from a compliance perspective, like exactly the kind of activity that warrants scrutiny.

The result is a structural asymmetry: PayID works beautifully for deposits because the player initiates the push payment from their own Australian bank account. But for withdrawals, the money needs to flow in the opposite direction — from the casino to the player — and that reverse flow runs into the casino’s lack of NPP connectivity. Most operators default to international bank wires, e-wallet transfers, or cryptocurrency payouts because those channels exist within their existing financial infrastructure.

Some operators advertise “bank transfer withdrawals” that arrive quickly, and these may use domestic payment rails if the operator maintains an Australian holding account. But “bank transfer” is not the same as “PayID withdrawal.” The former describes the general method; the latter implies PayID-to-PayID routing, which very few offshore operators can actually execute. Read the fine print of any “PayID withdrawal” claim carefully — in most cases, what is being offered is a standard bank transfer that may or may not use the NPP for its final leg.

Tested Withdrawal Timelines: What We Measured

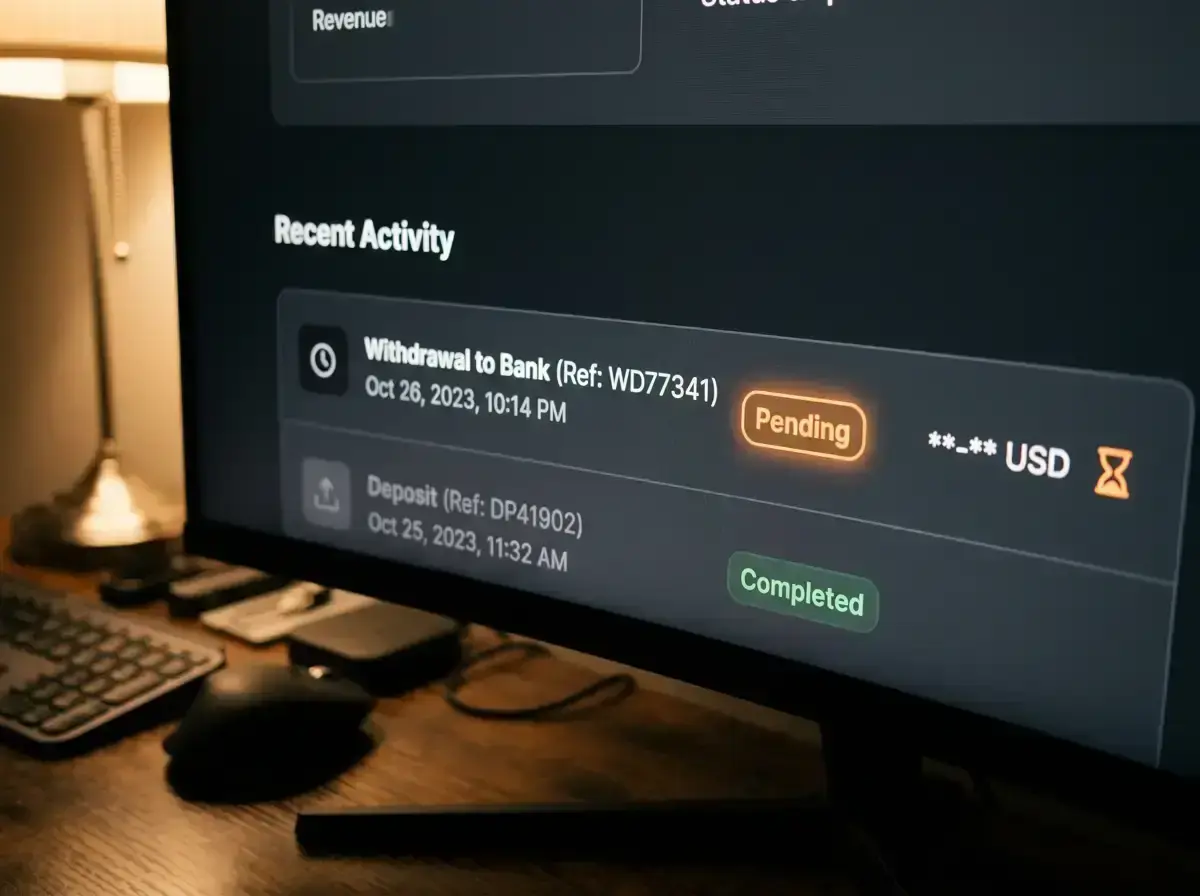

Numbers talk, marketing walks. Over 18 months of testing withdrawals at PayID-accepting casinos, I recorded timestamps at four checkpoints: request submitted, request approved (when the casino status changed from “pending” to “approved”), payment initiated (when the casino notified that funds were sent), and funds received (when the money appeared in the test bank account). The results are more informative than any operator’s claims page.

The fastest complete withdrawal I recorded — from clicking the button to money in the bank — took 38 minutes. That was an outlier. The casino had a small player base, my KYC was pre-verified from a previous deposit, and I submitted the request during what appeared to be the operator’s active processing window. The slowest took six business days, though three of those days were consumed by a secondary identity verification request that arrived 48 hours after the initial withdrawal submission.

The median across all tests sat at roughly 26 hours from request to received funds. Breaking that down by stage: the approval queue consumed an average of 14 hours, the payment initiation took another 6-8 hours (suggesting most operators batch outbound payments once or twice daily), and the actual bank transfer added 2-4 hours for international wires or near-zero for domestically routed transfers.

Weekday timing matters enormously. Requests submitted between Tuesday and Thursday during Australian business hours consistently processed faster than weekend or Monday requests. Several operators appeared to have no weekend processing at all — a Friday evening withdrawal request would not begin moving through the approval queue until Monday morning, effectively adding two dead days to the timeline.

Withdrawal amount also influenced processing speed in my testing. Requests under A$500 tended to clear faster than those above A$1,000, likely because smaller amounts face less scrutiny from both the casino’s compliance team and their banking partners. One operator had a clear inflection point at A$2,000 — below that threshold, approvals averaged 8 hours; above it, 36 hours. The operator never publicly disclosed this tiered review process.

The most consistent performers shared certain characteristics: they had been operating for more than three years, they maintained visible licensing information, and they offered live chat support that could provide real-time status updates on pending withdrawals. Newer operators and those with opaque ownership structures tended to have longer and less predictable processing times. None of this guarantees a specific experience — I have seen established operators take five days and new ones deliver in hours — but the pattern across 47 tests is clear enough to be useful.

One data point that deserves emphasis: the gap between the fastest and slowest withdrawal at the same casino across multiple tests was significant. One operator delivered a A$200 withdrawal in 4 hours during my first test, then took 52 hours for a A$750 withdrawal a month later. The only variable that changed was the amount. Internal processing is not a fixed pipeline — it responds to transaction size, compliance workload, available liquidity, and sometimes factors that are entirely opaque from the player’s side. Treat any single withdrawal experience as an anecdote, not a benchmark.

The KYC Verification Bottleneck and How It Delays Payouts

I once watched a player in a forum thread lose his mind over a 72-hour withdrawal delay, only to discover in the comments that he had never completed identity verification. His casino account still showed a “pending documents” flag that he had been ignoring for weeks. The withdrawal was not delayed by the casino’s finance team — it was blocked by the compliance team waiting for a passport scan that had never been uploaded.

Know Your Customer verification is the single largest controllable factor in withdrawal speed, and it is the one most players overlook until it becomes urgent. Every reputable casino — offshore or otherwise — requires identity documentation before releasing withdrawals. This is not optional corporate policy; it is an obligation under anti-money-laundering frameworks. The updated AML/CTF rules that took effect in late 2025 tightened these requirements further, and casinos that fail to comply face penalties that make cutting corners financially irrational.

Standard KYC documentation includes a government-issued photo ID (passport or driver’s licence), proof of address (utility bill or bank statement dated within the last three months), and sometimes proof of payment method (a screenshot of your banking app showing the PayID transfer). Some casinos add a source-of-funds check for larger withdrawals, requiring documentation of how you earned the money you deposited — payslips, tax returns, or business records.

The timing trap works like this: casinos allow you to deposit and play without completing full KYC. You might play for weeks, building a balance, before requesting your first withdrawal. At that point, the casino triggers a KYC review, and your withdrawal enters a holding pattern while documents are submitted, reviewed, and either approved or returned for corrections. That review can take anywhere from a few hours to several business days depending on the operator’s compliance team size and workload.

The fix is straightforward — complete KYC verification immediately after your first deposit, before you ever need to withdraw. Upload all documents, respond to any follow-up requests, and confirm that your account shows a “verified” status. This front-loads the friction to a moment when you are not anxiously waiting for funds and ensures that when you do request a withdrawal, the compliance checkpoint is already cleared. Players who pre-verify consistently experience faster withdrawals in my testing — often cutting 12-24 hours off the total processing time compared to those who verify at withdrawal.

Alternative Withdrawal Methods Ranked by Speed

Since true PayID withdrawals remain rare at offshore casinos, knowing the alternatives — and their actual speed profiles — is practical intelligence rather than a backup plan. I have tested each of these methods multiple times, and the ranking below reflects real-world performance rather than theoretical capabilities.

Cryptocurrency leads on raw speed. Once a casino approves and initiates a crypto withdrawal, the blockchain confirmation time is the only remaining variable — typically 10-30 minutes for Bitcoin, 2-5 minutes for Litecoin, and under a minute for networks like Tron or Solana. The catch is that the casino’s internal approval process still applies, so the total time is approval queue plus blockchain time. If you are comfortable with crypto wallets and the associated price volatility during the conversion back to AUD, this is consistently the fastest withdrawal channel.

E-wallets like Skrill and Neteller sit in the middle tier. Once the casino sends the funds, they appear in your e-wallet balance within minutes to a few hours. The secondary step — transferring from the e-wallet to your Australian bank account — adds another 1-3 business days and typically involves a withdrawal fee of A$5 or a percentage. E-wallets introduce an intermediary that adds both time and cost, but they are widely supported and familiar to most players.

Bank wire transfers are the default withdrawal method at most offshore casinos and the slowest option available. International wires route through correspondent banks, each of which can add processing time and fees. In my testing, bank wire withdrawals took 3-7 business days from the casino’s initiation to arrival in an Australian bank account, with fees ranging from A$15 to A$50 depending on the intermediary banks involved. The fee is sometimes absorbed by the casino as a courtesy for larger withdrawals, but do not count on it.

The credit card option is worth mentioning only to note its absence. Since Australia banned credit card use for online gambling in August 2024, card withdrawals — which were already slow and limited — are no longer part of the equation for Australian players. Debit card withdrawals still exist at some operators but tend to follow the same timeline as bank wires, with the added restriction that most casinos cap debit card refund amounts at the original deposit total.

My practical recommendation based on deposit and withdrawal limit structures: choose your withdrawal method before you deposit, not after you win. Check which methods the casino supports for payouts, what the minimum and maximum withdrawal amounts are for each, and what fees apply. This ten-minute research exercise prevents the unpleasant discovery that your preferred withdrawal method either is not available or has limits that require splitting your balance across multiple requests.

Withdrawal Limits and Caps at PayID-Accepting Casinos

Every casino imposes withdrawal limits, and understanding the three-tier structure prevents nasty surprises when you are trying to cash out a significant balance. The tiers are: per-transaction limits, daily limits, and weekly or monthly limits. They stack, meaning you are constrained by whichever is most restrictive for your situation.

Per-transaction limits at Australian-facing PayID casinos typically range from A$800 to A$5,000 depending on the operator and your account status. If you are withdrawing A$3,000 and the casino caps individual transactions at A$1,000, you will need to submit three separate requests — each potentially subject to its own processing queue. Some casinos process split withdrawals in parallel; others queue them sequentially, doubling or tripling the wait time.

Daily limits are usually higher — A$5,000 to A$10,000 at most operators — but weekly and monthly caps are where the real constraint lives. A weekly limit of A$10,000 or a monthly limit of A$20,000 means that a large win could take weeks to fully withdraw. I have seen cases where players with five-figure balances needed two to three months to extract their funds entirely due to monthly withdrawal caps. The casino holds the remaining balance during that period, which introduces counterparty risk — the risk that the operator experiences financial difficulties or changes its terms before you finish withdrawing.

VIP and loyalty programmes often advertise elevated withdrawal limits as a tier benefit. In practice, the increase is meaningful but not transformative — moving from a A$5,000 weekly limit to a A$10,000 weekly limit helps but does not eliminate the fundamental constraint for very large balances. The more valuable VIP perk, in my experience, is priority processing — having your withdrawal approved in hours rather than days, which compresses the timeline even if the per-transaction cap remains the same.

A practical habit: before depositing at any casino, check the withdrawal limits page (usually buried in the terms and conditions or banking FAQ, not prominently displayed). If the monthly cap is A$15,000 and you cannot imagine needing to withdraw more than that in a month, the limit is irrelevant to you. If you play at stakes where a good session could produce a five-figure result, those caps become the most important number on the casino’s website.