Last year I opened an account at a casino that advertised “A$5 minimum deposits” right on the homepage. I transferred exactly five dollars through PayID, watched it land in my balance within seconds, and then discovered I needed A$20 to activate the welcome bonus and A$10 more to meet the pokies minimum bet multiplied across enough spins to make the session worthwhile. That five-dollar minimum was technically real, but practically useless. Minimum deposits at PayID casinos sound straightforward until you run into the layered requirements that sit behind the headline number.

The real floor for a meaningful deposit depends on three separate thresholds stacked on top of each other: the casino’s own minimum, your bank’s minimum transfer amount for PayID, and the bonus activation requirement if you want promotional credits. Understanding where each threshold sits — and how they interact — is the difference between a controlled entry and an accidental overspend. The wholesale cost of processing a single NPP transaction has dropped from $0.39 in 2019 to roughly $0.04 in FY25, which means the infrastructure itself imposes almost zero friction on small transfers. The friction comes from the operators and the bonus terms.

Casino-Set Minimum Deposits: A to A Range

I spent a week in early 2026 logging the stated minimum deposit for PayID at over a dozen offshore casinos accepting Australian players. The range was wider than I expected. A handful listed A$5 as the absolute floor. Most sat at A$10. A few — particularly those targeting high-volume players — set the bar at A$20 or even A$30. The number changes depending on the payment method too; the same casino that accepts A$5 via PayID might require A$20 for a card deposit, because card processors charge a flat fee that makes tiny transactions unprofitable.

PayID sits in a sweet spot for low-entry deposits precisely because the transaction cost on NPP rails is negligible. Casinos are not absorbing a percentage-based fee or a flat gateway charge, so there is no financial incentive to inflate the minimum. When a casino sets its PayID minimum at A$20 instead of A$5, the reason is almost always operational — they want to reduce the volume of micro-deposits that generate support tickets without producing meaningful play. It is a customer-management decision, not a cost-recovery one.

One detail that trips people up: the minimum shown on the cashier page applies to the deposit method, not to the account. If you deposit A$5 via PayID and then try to use a different method later, the second method’s minimum applies independently. These are not cumulative. Each deposit is its own transaction with its own floor.

The stated minimums also shift without notice. I have seen casinos quietly raise their PayID floor from A$5 to A$10 between quarterly site updates. Always check the cashier at the moment you intend to deposit rather than relying on a number you saw a month ago.

Bank-Side Minimums for PayID Transfers

A mate of mine tried to send A$1 through PayID from his Westpac account as a test. It went through. He tried the same from a different bank and hit a A$1 minimum that effectively meant zero friction. Most of the Big Four — CommBank, ANZ, NAB, Westpac — allow PayID transfers starting from one cent, though some mobile app interfaces round up to a dollar minimum for practical reasons. Credit unions and smaller institutions occasionally set their own floors, but these rarely exceed A$5.

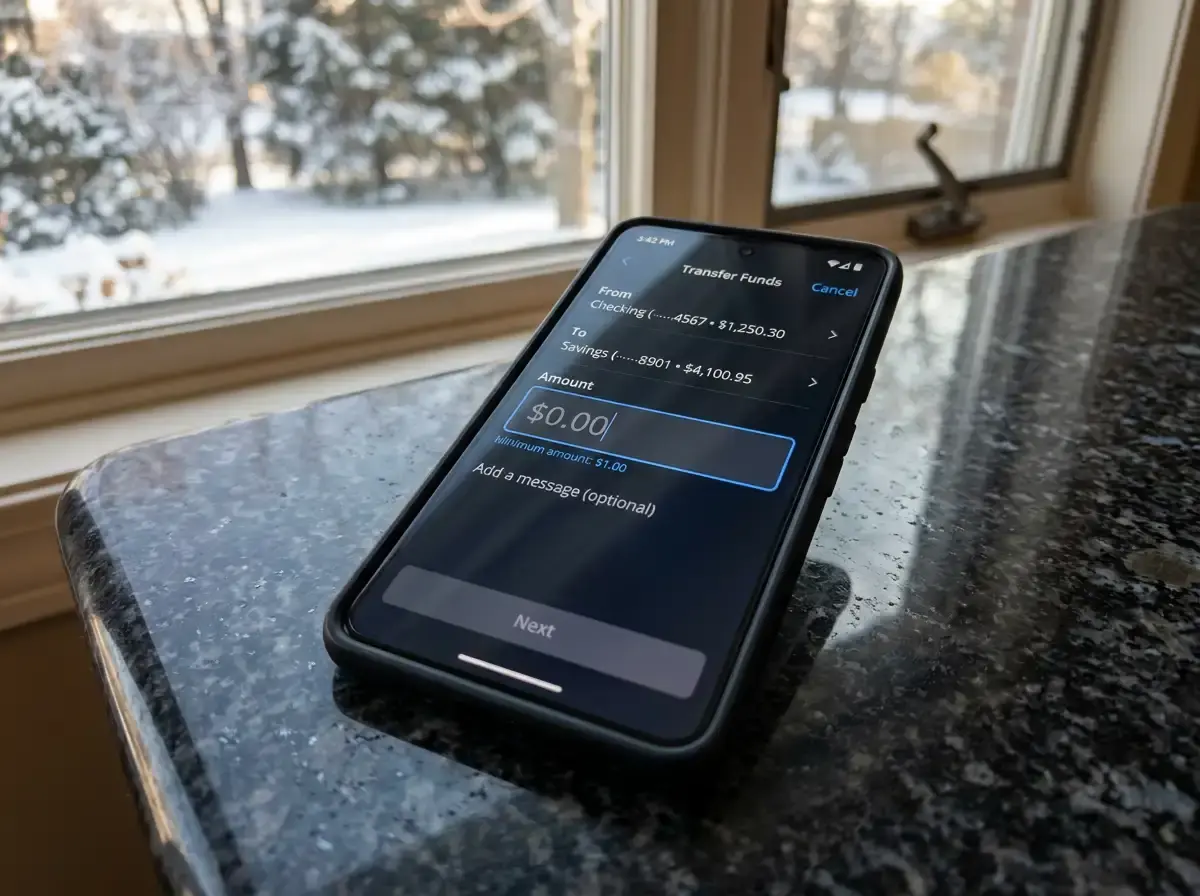

The bank-side minimum is almost never the binding constraint. PayID adoption itself has surged — ABA CEO Anna Bligh noted that PayID’s share of all payments jumped from 12% in early 2021 to nearly 20% by late 2022, and the trajectory has only steepened since. That growth means banks have every reason to keep PayID accessible at the lowest possible entry point. Where it gets interesting is in daily transfer caps. Some banks let you send up to A$1,000 per day through PayID by default, while others set the ceiling at A$2,000 or higher. If you are depositing at the minimum, the cap is irrelevant. But if you plan to start small and top up later in the same session, hitting the daily cap can be an unexpected blocker. Your bank’s app usually displays the remaining daily limit somewhere in the transfer confirmation screen — worth checking before you assume a second transfer will go through.

There is another wrinkle that rarely gets mentioned. Some banks flag outbound PayID transfers to unrecognised recipients and impose a temporary hold — typically 24 hours — on the first transaction. This is a fraud-prevention measure, not a minimum-deposit rule, but it can look like one if your A$5 transfer sits in limbo overnight. After the first successful transfer to a given PayID, subsequent ones clear instantly.

Minimum Deposit vs Bonus Activation Thresholds

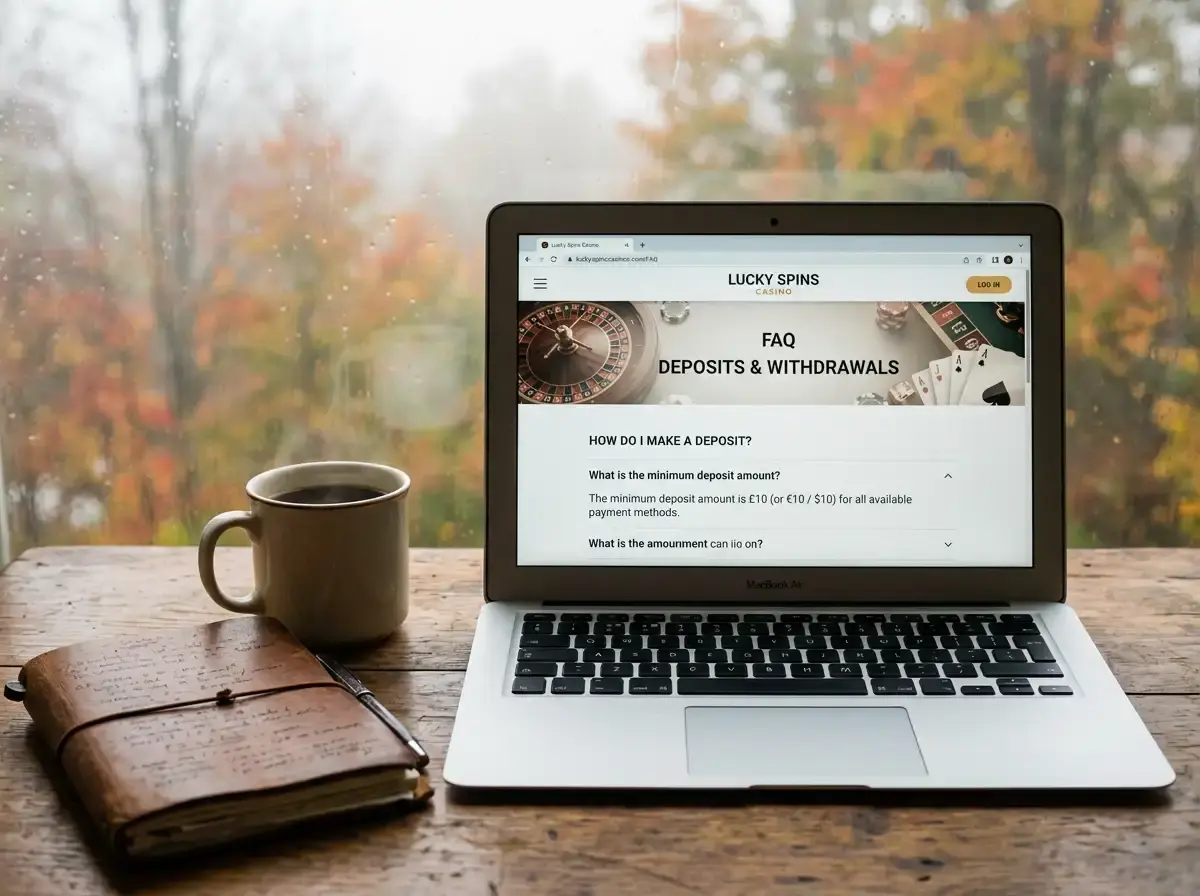

Here is where the real gap opens up. I tracked bonus terms across eight PayID-friendly casinos and found that not a single one activated its welcome offer at the stated deposit minimum. The pattern was consistent: deposit minimum A$10, bonus activation A$20. Deposit minimum A$5, bonus activation A$20 or A$30. The lowest bonus activation threshold I found was A$15, and that was an outlier.

This creates a two-tier system. You can technically deposit A$5 and play with just your own funds, no strings attached. Or you can deposit A$20-plus, trigger the bonus, and immediately inherit wagering requirements that might demand 30x to 50x playthrough on the combined deposit-plus-bonus amount. Neither option is inherently better — they suit different goals. The minimum deposit with no bonus is genuinely low-friction entry. The bonus-qualifying deposit is a different proposition entirely, one that commits you to a specific volume of play before withdrawal.

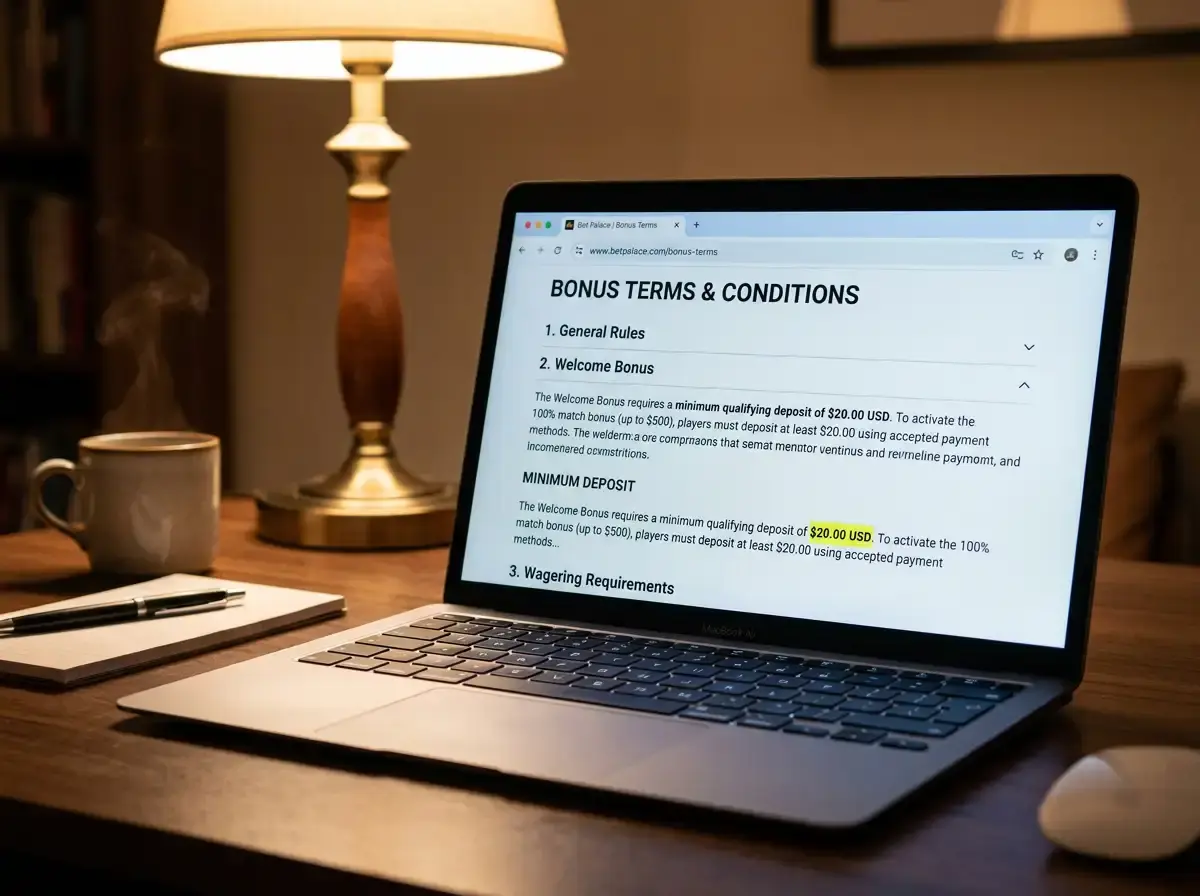

Watch for the “maximum bonus” ceiling too. A 100% match up to A$500 sounds generous until you realise the minimum qualifying deposit is A$20, which gives you A$20 in bonus funds subject to 35x wagering — that is A$1,400 in total bets required to clear twenty dollars of bonus money. The maths matters more than the headline. Since 60.3% of Australian adults participated in some form of gambling in 2024, the audience for these offers is enormous, and operators design bonus structures to maximise engagement across that wide base, not to reward the minimum depositor.

Is a Minimum Deposit Worth It? Bankroll Math

I ran the numbers on a A$5 deposit playing pokies with an average bet of A$0.20 per spin. That gives you 25 spins before your balance hits zero — assuming no wins, which is the planning baseline. Average session length at that rate: about three minutes. With a 95% RTP slot, your expected balance after 25 spins is roughly A$4.75, giving you maybe 24 more spins, then 23, and so on until variance finishes you off. Realistically, a A$5 bankroll sustains 10 to 15 minutes of play under normal conditions.

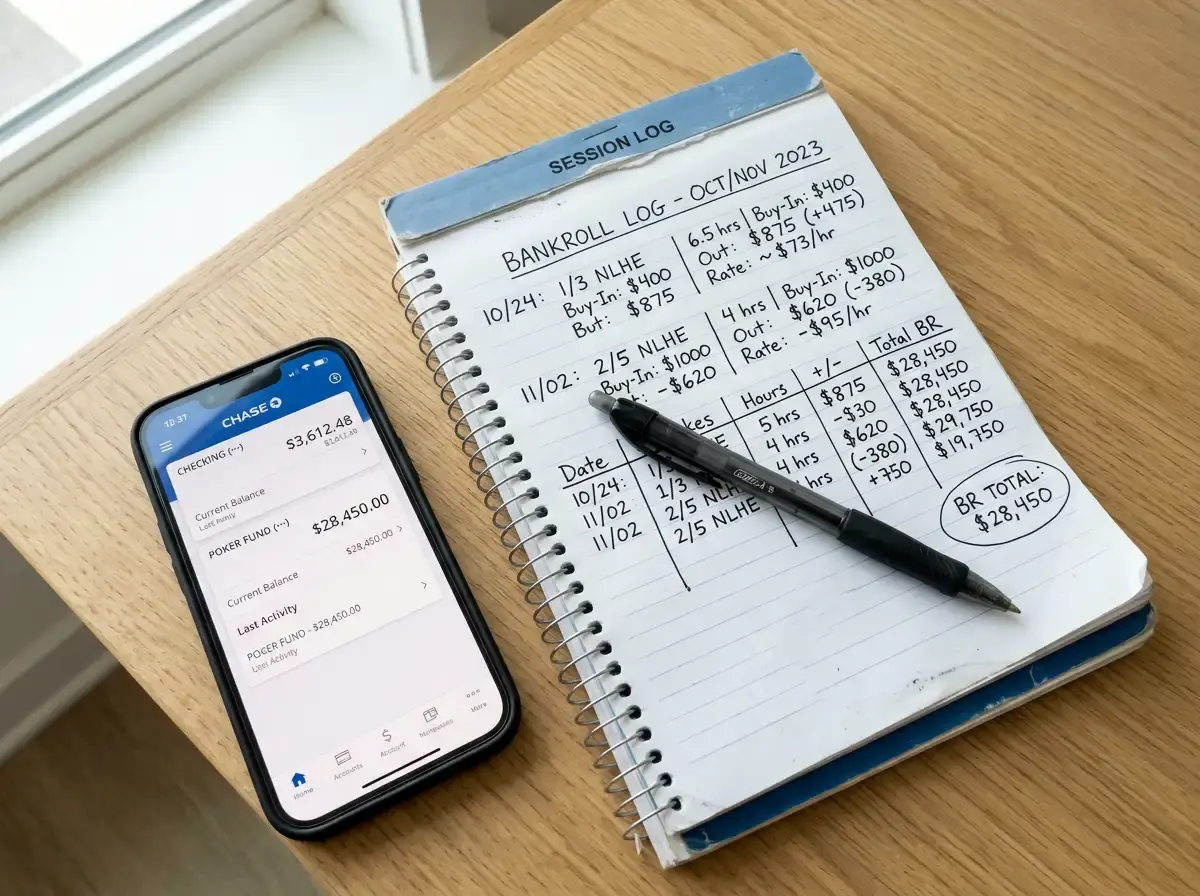

Australians lost an average of A$1,555 per adult on gambling in the 2022-23 financial year, a figure that has only climbed since. A minimum deposit strategy is one of the few genuine friction points that can slow spending velocity — but only if you treat it as a session cap rather than a starting point for top-ups. The moment a A$5 deposit turns into “just one more fiver,” the minimum loses its protective function.

For players using minimum deposits as a budgeting tool, the most effective approach is to set a daily transfer limit in your banking app that matches your intended session spend. PayID makes this easy because each transfer is discrete and trackable in your banking history. Unlike card deposits that might batch or appear as a generic merchant charge, a PayID transfer to a specific recipient shows up immediately with the exact amount. That transparency around transaction limits turns the deposit minimum from a marketing number into an actual spending boundary.

Where the True Floor Sits

Strip away the marketing and the real minimum deposit at a PayID casino is not the number on the cashier page. It is the sum of three questions: what is the lowest amount the casino will process, what does your bank allow as a minimum transfer, and what are you actually trying to achieve with the deposit? If you want bonus funds, your floor is the bonus activation threshold — typically A$20 to A$30. If you want a no-strings session, the floor is whatever the cashier says, often A$5 to A$10. If you want enough runway to make the session meaningful, the floor is your target session length multiplied by your average bet size.

The NPP infrastructure has done its job. Transaction costs are negligible, processing is instant, and there is no technical reason why a A$1 deposit cannot work. Every barrier above that is a business decision by the casino or a personal budgeting choice by you. Knowing which layer is setting your actual minimum means you are making the deposit on your own terms, not on the operator’s.